True lifelong financial planning for the serious business of life.

True lifelong financial planning

for the serious business of life.

True lifelong financial planning for the serious business of life.

True lifelong financial planning

for the serious business of life.

Category: Investment management

The Clarion Investment Committee met on Wednesday, 20 May. The following notes summarise the main points of consideration in the Investment Committee discussions but have been updated to include commentary on recent events and the wider implications for financial markets.

Please click here to access our May Stock Market & Economic Commentary written by Clarion Group Chairman, Keith Thompson.

Our investment philosophy is guided by proven financial research, applied with care by our in-house Investment Committee. We do not chase trends or make predictions. Instead, we rely on evidence, structure, and oversight to manage wealth responsibly over the long term.

We focus on what can be controlled: diversification, discipline, and costs. This allows us to create efficient portfolios designed to weather uncertainty and deliver the returns that markets provide.

Our approach is built on five enduring principles, which together form the foundation of our Investment Philosophy.

Each of the five philosophy pillars reflects our commitment to managing your wealth with clarity, discipline, and care.

1) Evidence-based investing. Disciplined diversified portfolios deliver better long-term outcomes than chasing the latest market trend.

2) A systematic process. A structured repeatable process designed to remove guesswork and emotion.

3) Cost efficiency. We carefully select cost-effective investment solutions without compromising quality.

4) Independent oversight. Every decision is reviewed and challenged by our in-house Investment Committee, supported by Margetts Fund Management and Dynamic Planner.

5) A responsible perspective. Identifying risks and opportunities that could affect your wealth in the years to come and building resilience into client portfolios.

Financial markets continue to face elevated geopolitical risks, mainly centred around the policies implemented by US President Donald Trump since he was inaugurated for a second time on 30 January 2025.

Initial policies focused on international trade with the imposition of US trade tariffs, dubbed ‘trade wars’ by market commentators, and more recently, threats to the sovereignty of Greenland, special military intervention in the removal of the Venezuelan President, Nicolas Maduro, a full-scale military attack on Iran, with Cuba threatened as the next target.

Despite all these major incidents and the continued Russian military conflict in Ukraine, which began on 24 February 2022, investment markets remain positive, perhaps confounding the expectations of many investors.

During the 1950s, the phrase ‘stock markets climb walls of worry’ was coined to describe the observation that markets generally rose despite persistent trade wars, geopolitical tensions and military conflicts. Although this phrase dropped out of regular use from the late 1980s, recent events suggest a resurgence has occurred.

The factors driving this historically and today are the inflationary effects of global risks, which generally drive up ‘real’ assets (e.g. equities) and create a headwind for cash and fixed interest assets. The key to this observation continuing is that GDP growth remains positive and inflation does not lead to interest rates rising enough to trigger a recession.

For example, the growth of the UK economy from 2023 to 2025 (inclusive) was 6.3% according to ONS data and is measured in real terms (adjusting for inflation). However, the nominal growth, measured in sterling, was far higher at 23%, as this was a period of elevated inflation. As businesses have been operating in an economy that has grown nearly a quarter in three years, their revenue and profits have increased significantly in aggregate, leading to higher market valuations and higher future earnings expectations.

Generally, low and falling inflation favours cash and fixed interest investments, as occurred in the decade following the global financial crisis in 2008/9. Moderate inflation favours real assets such as equities, as is currently being experienced. If inflation becomes too high, it erodes the value of most assets and can lead to a breakdown of social cohesion, as occurred most notably in the Weimar Republic in the 1920s due to hyperinflation.

The current conditions of high government debt, de-globalisation, special military actions and diminishing trust in the global rules-based order are expected to maintain elevated inflation over the next cycle, which likely began in 2022, as Covid restrictions were eased, Russia invaded Ukraine, and global inflation began to rise. The previous cycle of low interest rates and inflation began in 2008 with the collapse of Lehman Brothers and lasted for 14 years. The current cycle could be of a similar duration, so we are potentially only at an early stage.

The decision of Israel and the US to attack Iran has further increased geopolitical risks and led to the closure of the Strait of Hormuz, which is significant as 20% of global oil supplies transit through this area. Unsurprisingly, this has concerned some investors, leading to profit taking and capital flowing into safer assets, although this could be a ‘second-order effect problem’ where the initial action makes sense but fails once the longer-term effects are considered.

If the Iran conflict continues with the Strait of Hormuz closed for the foreseeable future, how much will the cost of oil rise and will it trigger a global recession? During the invasion of Ukraine by Russia in 2022, there were similar concerns, yet even though the military action remains ongoing, the effect on oil prices was temporary and supply chains quickly adapted to normalise prices.

Following the recent spike, oil is now below $100 per barrel, being lower than the peak reached in 2022. Oil supply globally is plentiful, with the US production increasing dramatically, potential new supplies from Venezuela, technology increasing yields from old oil fields and some of the Gulf oil transiting through land pipelines, avoiding the closed Strait. Before the Iran war, the world had an oversupply of oil estimated at around 4 billion barrels per day, or approximately 4% of total consumption. Therefore, whilst a higher price is expected to continue, past experiences and the evident supply flexibility are expected to avoid a full-blown energy crisis, whilst the Strait will also re-open at some point, be that sooner or later.

During the energy crisis of the 1970s, the demand for oil was considered inelastic, that is to say, the demand remained the same regardless of price, as there were no other material energy options available. In modern times, there are more sources of energy available, with the UK now generating more than 50% of electricity from non-carbon sources, so the dependence on oil is slowly easing. Recent uncertainty over oil supplies will continue to encourage diversification of energy generation, reducing future dependency further.

Henry Ford famously stated that half of the money he spent on advertising was wasted, he just didn’t know which half. As the capital spending around artificial intelligence (AI) continues to spiral higher, it is certain that some of this capital is being misallocated; we just don’t know which capital!

Estimates for the MAG 7 (Microsoft, Alphabet, Amazon, Meta, Nvidia, Apple and Tesla) capital investment into AI infrastructure in 2026 are around $700 billion, being only around $200 billion less than the US annual military budget. If the current year-on-year trend continues, the spending on AI will exceed the pre-Iran US military budget next year and is akin to a significant fiscal stimulus.

The intense spending in this area belies the anxiety of Mag 7 CEOs that AI is an existential threat to those firms that do not develop capability in this area. Just as Nokia and RIM (Blackberry) were destroyed by the smartphone, Microsoft, for example, could suffer the same fate if it does not participate in the AI revolution. The entire sector currently enjoys lofty valuations, and predicting the winners and losers is particularly difficult, given that the potential of the emerging technology is not yet fully understood.

Outside of the big technology firms, the day-to-day benefits for businesses are becoming apparent. Just as robotics revolutionised the efficiency of manufacturing processes, AI is showing similar benefits for streamlining administration, governance, research, and many other applications. Businesses and governments have long required office blocks full of people conducting administrative functions, and AI is now greatly increasing the efficiency of these activities.

Within medium and smaller size businesses, especially where valuations are more attractive, these productivity gains should provide a long-term profitability tailwind for those businesses that adopt the new technologies available.

It is notable that whilst the US is dialling up military interventions and threats over Greenland, Cuba, Venezuela and Iran, China is taking a more conciliatory approach. Politically, President Trump has seen Europe and other NATO allies stepping back from close US involvement, driven by the US-first policy introducing wide-ranging, unpredictable tariffs and US unilateral, unpredictable foreign policy decisions.

Despite pleas for help during the attacks on Iran, no other country has been prepared to offer support to the US and Israel, with President Trump unable to hide his anger. The collective ‘shoulder shrug’ of long-term allies when asked to assist the US in Iran, especially the UK as the most loyal historical US ally, shows the distancing and deterioration of the special relationship under President Trump.

China may be following the advice of the renowned military leader Napoleon Bonaparte, who said ‘Never interfere with an enemy while he’s in the process of destroying himself’, by keeping its distance from military conflicts and limiting its response to calling for diplomatic solutions. It is notable that China has been discussing more peaceful unification narratives towards Taiwan, talking about resuming cross-strait ties and increasing direct flights from mainland China. Given Russia’s invasion of Ukraine and the US attack on Iran, this could have emboldened China to also use military means to achieve its reunification goals, but they have taken a different approach. As confidence in the US deteriorates, China appears to be positioning itself as a trusted partner to increase political and trading links with countries that were previously US-focused. For example, Keir Starmer held talks with President Xi to bolster UK economic ties with China earlier this year.

In conclusion, this has been a positive period for global equity markets, which seems remarkable, at first glance, given the ongoing developments. The positive stock market performance is attributed to the inflationary effect of these developments, together with the huge stimulus from AI investment, the broad expected productivity gains from AI and accommodative central bank policies that are not inclined to raise interest rates.

The outlook remains positive for equities, which will continue to ‘climb walls of worry’, although the rotation from US stocks to other global markets seen since the beginning of President Trump’s second term, is expected to continue, due to failing trust amongst US trading partners and the alternative, mature political leadership shown by China.

We continue to hold reduced allocations to fixed interest investments, as these assets are negatively affected by rising inflationary pressure. Where held, the maturity profile is at the shorter end, as the inflationary effect is negligible, and the fixed rate offered is above the expected rate of inflation to provide a real return.

Allocations to the US are underweight due to higher valuations, the dominance of AI-driven stocks, and the difficulty in predicting which companies will achieve an economic return from their AI investments and how this will occur.

Weightings are diversified away from US assets in favour of UK, Europe, Asia and Emerging Markets, which are more attractively valued and expected to benefit broadly from AI as businesses find efficiencies through the implementation of this technology.

Holding a globally diversified portfolio of high-quality assets is important to provide resilience and grow the value of savings over the long term, and remains the appropriate method for allocation of investor capital. Cash is unattractive as inflationary pressures, although moderating, look to be structurally long term.

Clarion Funds:

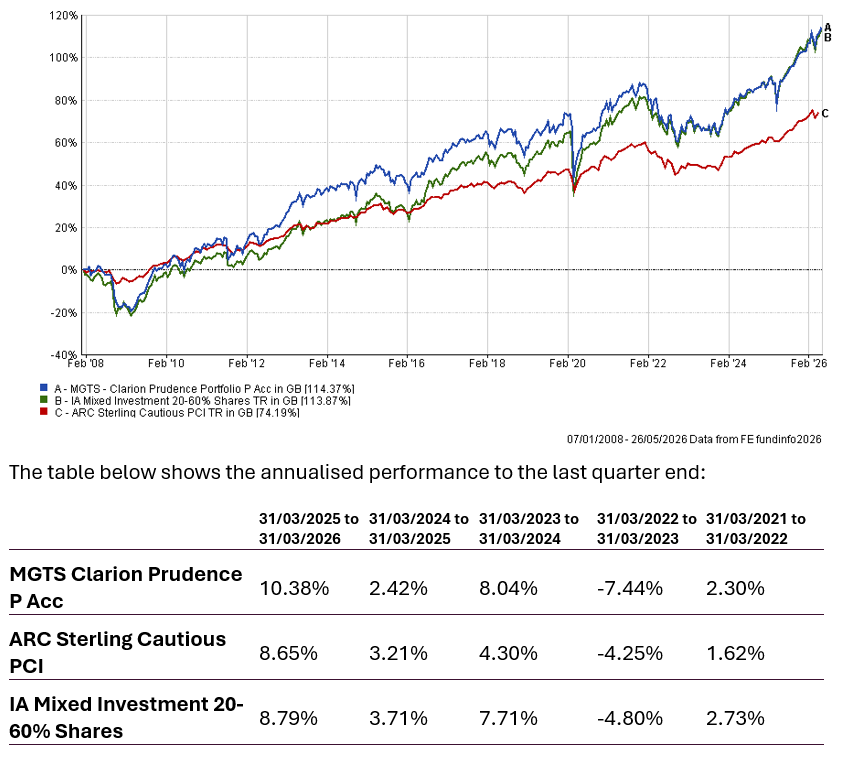

The chart below shows the historical performance of the Prudence Portfolio against a relevant benchmark since the start of the available data.

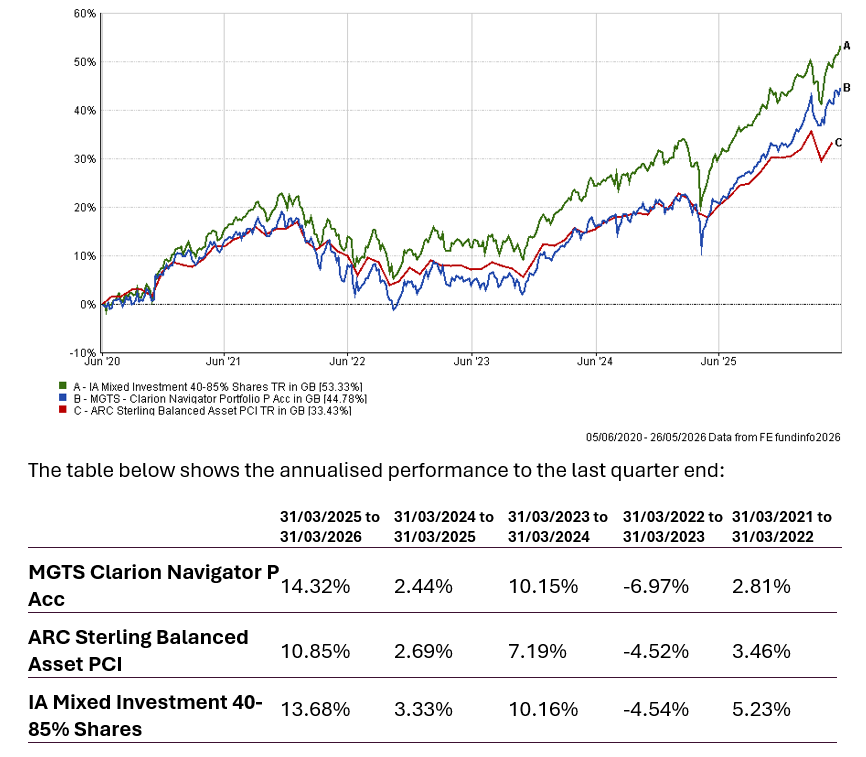

The chart below shows the historical performance of the Navigator Portfolio against a relevant benchmark since the start of the available data.

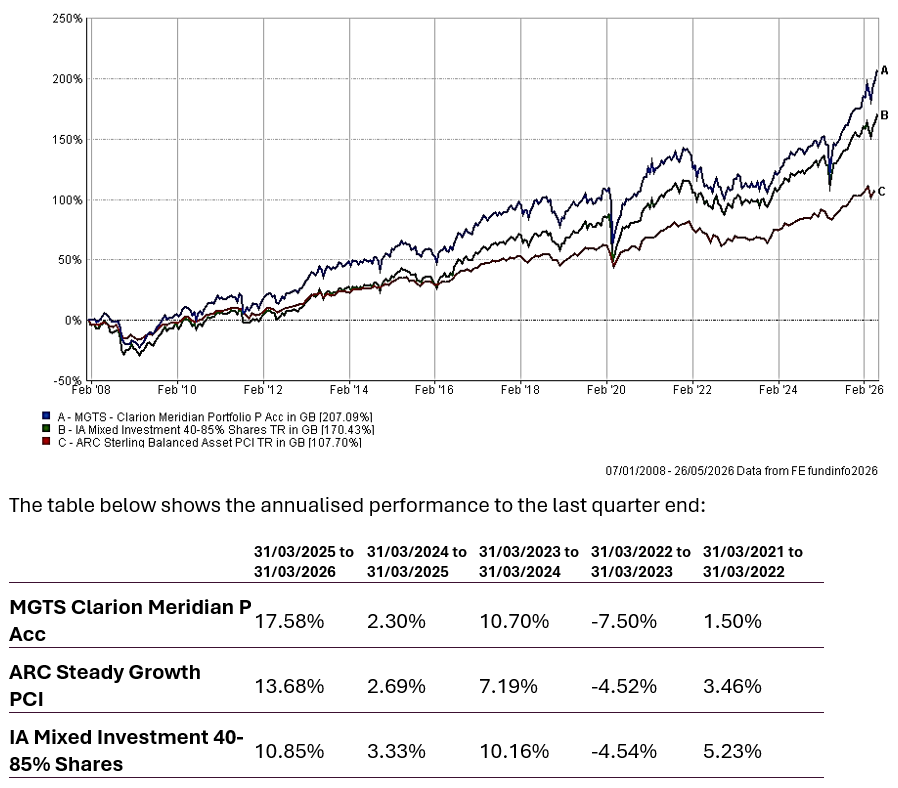

The chart below shows the historical performance of the Meridian Portfolio against a relevant benchmark since the start of the available data.

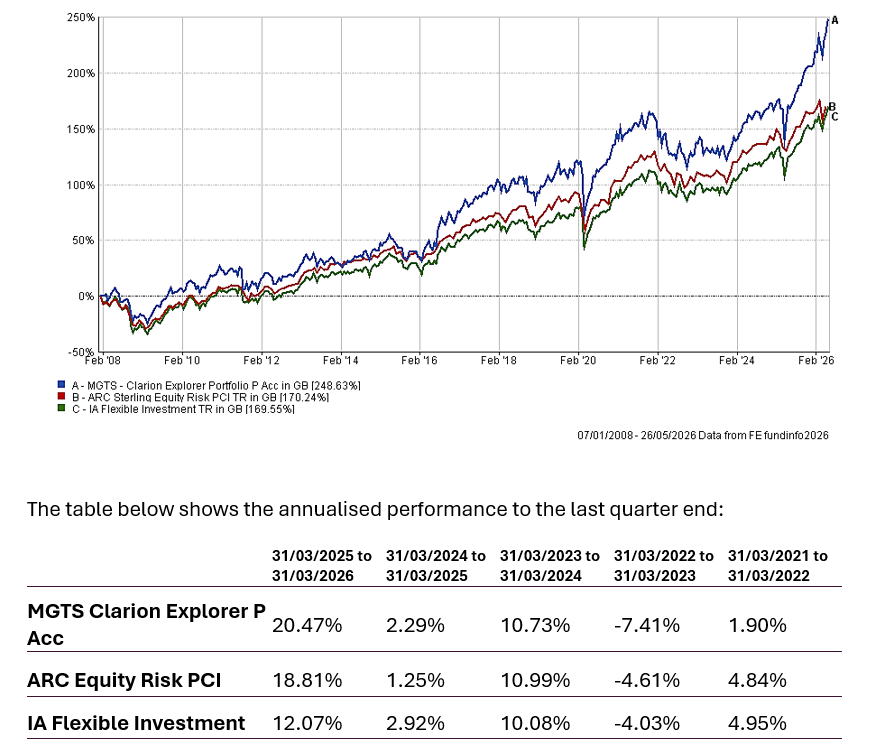

The chart below shows the historical performance of the Explorer Portfolio against a relevant benchmark since the start of the available data.

Keith W Thompson

Clarion Group Chairman

May 2025

Any investment performance figures referred to relate to past performance which is not a reliable indicator of future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments, and the income arising from them, can go down as well as up and is not guaranteed, which means that you may not get back what you invested. Unless indicated otherwise, performance figures are stated in British Pounds. Where performance figures are stated in other currencies, changes in exchange rates may also cause an investment to fluctuate in value.

The content of this article does not constitute financial advice, and you may wish to seek professional advice based on your individual circumstances before making any financial decisions.

If you’d like more information about this article, or any other aspect of our true lifelong financial planning, we’d be happy to hear from you. Please call +44 (0)1625 466 360 or email [email protected].

Click here to sign-up to The Clarion for regular updates.