The Clarion Investment Committee met on 11 December 2025. The following notes summarise the main points of consideration in the Investment Committee discussions but have been updated to include commentary on recent events and the wider implications for financial markets.

Please click here to access our December Stock Market & Economic Commentary written by Clarion Group Chairman, Keith Thompson.

The Clarion approach to investment management

Our investment philosophy is guided by proven financial research, applied with care by our in-house Investment Committee. We do not chase trends or make predictions. Instead, we rely on evidence, structure, and oversight to manage wealth responsibly over the long term.

We focus on what can be controlled: diversification, discipline, and costs. This allows us to create efficient portfolios designed to weather uncertainty and deliver the returns that markets provide.

Our approach is built on five enduring principles, which together form the foundation of our Investment Philosophy.

Each of the five philosophy pillars reflects our commitment to managing your wealth with clarity, discipline, and care.

1) Evidence-based investing. Disciplined diversified portfolios deliver better long-term outcomes than chasing the latest market trend.

2) A systematic process. A structured repeatable process designed to remove guesswork and emotion.

3) Cost efficiency. We carefully select cost-effective investment solutions without compromising quality.

4) Independent oversight. Every decision is reviewed and challenged by our in-house Investment Committee, supported by Margetts Fund Management and Dynamic Planner.

5) A responsible perspective. Identifying risks and opportunities that could affect your wealth in the years to come and building resilience into client portfolios.

Economic Commentary & Market Outlook

The following is a summary of the major events and economic news since the last Clarion Investment Diary.

Economics

- The US Federal Reserve (Fed) cut interest rates for the third consecutive time, to 3.5%-3.75%, noting an increased risk of a labour market slowdown. The decision was split, with two board members voting to hold rates while Stephen Miran, recently appointed by US president Donald Trump, advocated for a larger cut.

- The Bank of England (BoE) also cut interest rates by 0.25% to 3.75% bringing the base rate to its lowest level since February 2023. The move was widely expected, not least because the UK economy contracted by 0.1% in October amid increased business uncertainty in the run-up to the government’s Autumn Budget, and recent figures showed that UK inflation fell from 3.6% to 3.2% in November.

- UK credit card spending fell by 1.1% in November, the largest annual decline since February 2021, according to Barclaycard data, due to poor weather and households’ uncertainty ahead of the Autumn Budget.

- Despite declining card spending, UK pubs and bars have seen a surge in bookings over the Christmas period, with major pub chains reporting higher sales compared with the same period last year.

- UK banks said they could be exposed to legal risks from the UK government’s plans to use approximately £8 billion of frozen Russian assets, which they hold to provide loans to Ukraine, the FT reports.

- Investors now assign a greater probability to interest rates rising in the Euro area next year than falling, likely in part due to better-than-expected economic activity and pockets of stubborn inflation. Rising rates in the Euro area would likely add further downward pressure to the US dollar.

- The BoE announced plans to cut operating costs to boost investment in its economic modelling capacity, as part of measures to address the outcomes of the review into the central bank by former US Fed chair Ben Bernanke.

- France’s parliament narrowly voted in favour of the government’s social security budget, which includes suspending French president Emmanuel Macron’s previously proposed plans to increase the retirement age. Negotiations over the government’s budget plans are still ongoing.

- China’s trade surplus in goods surpassed £1 trillion so far this year, the highest amount on record. The decline in goods exported directly to the US was more than offset by exports to other regions, in particular other Asian countries

- Private credit lending to emerging markets reached a record $18 billion this year, filling a gap left by declining bank loans, according to the Global Private Capital Association.

Business

- US president Donald Trump said he will allow US tech company Nvidia to export its H200 chips to China, which had previously been restricted due to national security concerns.

- Paramount announced a $108 billion hostile bid for the Warner Bros Discovery media company, in an attempt to outmanoeuvre Netflix’s $72 billion agreement to buy Warner Bros’ film and TV studios business. Mr Trump said Netflix’s takeover “could be a problem” due to the business’s combined market share.

- Microsoft and Amazon announced investment in India worth a combined total of over $50 billion over the coming years, as US tech companies look to expand AI and cloud services in the country.

- Disney announced a $1 billion investment into US tech company OpenAI that would allow its characters to be used on OpenAI’s AI video generation platform, Sora.

- Online messaging website Reddit filed a lawsuit in Australia to overturn the government’s social media ban for children, saying it interferes with free political communication.

- US car manufacturer Ford agreed a partnership with French rival Renault, whereby Renault will build two new, Ford-designed EV models in Europe in an attempt to boost its competitiveness in Europe against Chinese rivals.

- The UK Parliamentary Contributory Pension Fund faces criticism for having less than 3% of its equity portfolio invested in UK shares, lower than private sector funds and contrasting with the government’s plans to boost investment into UK assets.

- The NHS said it is facing a “worst-case scenario for this time of year” due to a record high number of hospital patients with flu in November, a record number of A&E visits and the resident doctors’ strike.

Global & Political Developments

- Ukrainian president Volodymyr Zelenskyy said he would give up on demands for Ukraine to become a member of NATO in exchange for US and European security guarantees. Ukraine would join the EU next year, according to the latest draft peace proposal from Ukraine and European officials, the FT reports.

- Mr Zelenskyy also said he would be ready to hold presidential elections within the coming months if European nations and the US could ensure security. Mr Zelenskyy previously faced criticisms from the US for not holding elections when his term was due to end last year, despite elections being postponed under martial law.

- Lithuania declared a nationwide “emergency situation” following the entry into its airspace of hundreds of giant weather balloons carrying smuggled cigarettes from Belarus. Belarus’s leader is a close ally of Vladimir Putin, and the balloon incursions appear to be an attempt to destabilise Lithuania.

- Russia’s central bank is suing the Euroclear depository system for freezing €185 billion in frozen Russian assets, amid attempts by the EU to use the assets to fund a €90 billion loan to Ukraine.

- NATO chief Mark Rutte said that “we must be prepared for the scale of war our grandparents and great grandparents endured” and called for greater preparations by NATO members for a war with Russia.

- Mr Trump labelled European economies as ‘decaying’ and called their leaders weak for failing to curb migration and end Ukraine’s war with Russia.

- The Trump administration announced plans for applicants who want to visit the US under the visa-waiver programme, which includes citizens from the UK and France, to disclose the past five years of their social media history.

- US military forces seized an oil tanker off the Venezuelan coast, escalating tensions between the nations. The Trump administration said the tanker was bound for Iran, which currently faces sanctions. Venezuela’s foreign office condemned the act as “international piracy”.

Macroeconomic Outlook and Investment Strategy

- 2025 has been a good year for stock markets, with performance defying pessimistic expectations around tariffs and trade wars.

- A key observation is that for a UK investor, the US market has underperformed the rest of the world this year, marking the first time this has occurred since the 2008-2009 global financial crisis.

- Historically, US outperformance has been driven by superior liquidity, which has consistently pushed valuations to a premium. This long-term trend may have started to break down.

- There is a view that the US may be entering a period of relative decline, with its global influence waning and creating a vacuum that China is starting to fill. US tariff policy is seen as an own goal that is difficult to reverse and ultimately benefits other manufacturing nations.

- From a valuation perspective, the US market is considered ‘very expensive’, whereas the rest of the world, including the UK, Europe, and emerging markets, is trading at ‘about average’ valuations, making these regions more attractive.

- A significant risk is the high level of expectation for AI-driven profits, which may not materialise. Much of the investment appears to be defensive or circular between major tech firms, and valuations in the sector look ‘toppy’.

- The global economy is in an embedded inflationary cycle, driven by prior monetary expansion and current wage pressures. In this environment, real assets such as equities are expected to perform well as cash loses purchasing power.

- The outlook for the bond market is cautious. Bond yields are considered less attractive than they appear on a real, after-tax basis. Long-dated government bonds are seen as particularly unattractive, with a prediction that the UK 10-year gilt could reach 6%.

- Corporate credit spreads are tight, but this is supported by strong corporate balance sheets. A developing risk is the potential for companies to overspend on AI infrastructure, with leverage just beginning to build in the system.

Portfolio and Fund Performance Review

- Portfolio adjustments were considered, including a review of the Asian allocation with a focus on funds from Jupiter and M&G, and a potential increase in non-US infrastructure to diversify away from the L&G fund’s heavy US exposure.

- The strategy to maintain a shorter duration stance in fixed income was reaffirmed due to concerns that increased government debt issuance and persistent inflation will continue to put upward pressure on the long end of the curve.

- The discussion highlighted that a key performance detractor has been the ‘manager benchmark misfit’, where the active funds held have underperformed the passive indices within the benchmarks, particularly in the US.

- However, it was noted that the underlying manager selection within each sector has been a positive contributor to performance.

- Analysed the Dimensional Emerging Markets core fund, noting its value tilt has caused it to lag behind growth-focused peers over the last year.

- Compared the performance of all funds against their IA sector benchmarks, observing that most have performed well, particularly Dimensional European Value, which has significantly outperformed.

- Highlighted the severe underperformance of the UK Buffettology fund, a previous holding which was sold in June 2022 due to concerns about performance, which has lost money over the past five years, contrasting it with the strong returns from Dimensional UK Value.

Action Points & Next Steps

- Adjust the Asian fund allocation. The decision was made to replace the Schroder Institutional Pacific fund with the M&G Asia fund across all portfolios to maintain desired China exposure whilst improving the performance profile.

- Adjust the infrastructure allocation. It was agreed to increase the holding in the BNY Mellon Global Infrastructure fund by 1%, funded by reducing the L&G Global Infrastructure Index fund, to lessen the portfolio’s concentration in the US.

Clarion Portfolio Funds

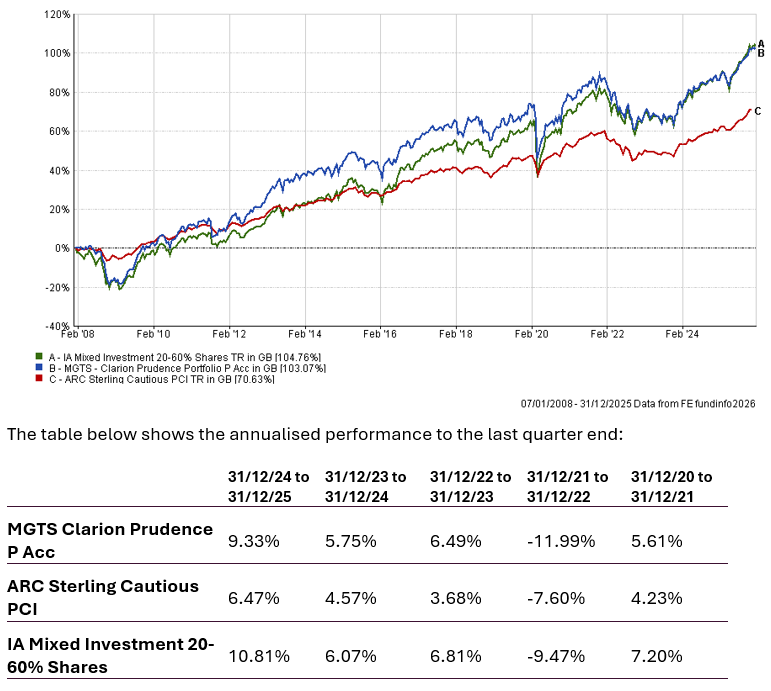

Prudence Fund

The chart below shows the historical performance of the Prudence Portfolio against a relevant benchmark since the start of the available data.

Changes to the Prudence Fund

Due to changes in the underlying strategic asset allocation, the following changes were made to the Prudence portfolio:

Equities

- L&G Global Infrastructure Index I Acc was decreased from 4.50% to 3.50%

- BNY Mellon Global Infrastructure Income F Acc was increased from 1.50% to 2.50%

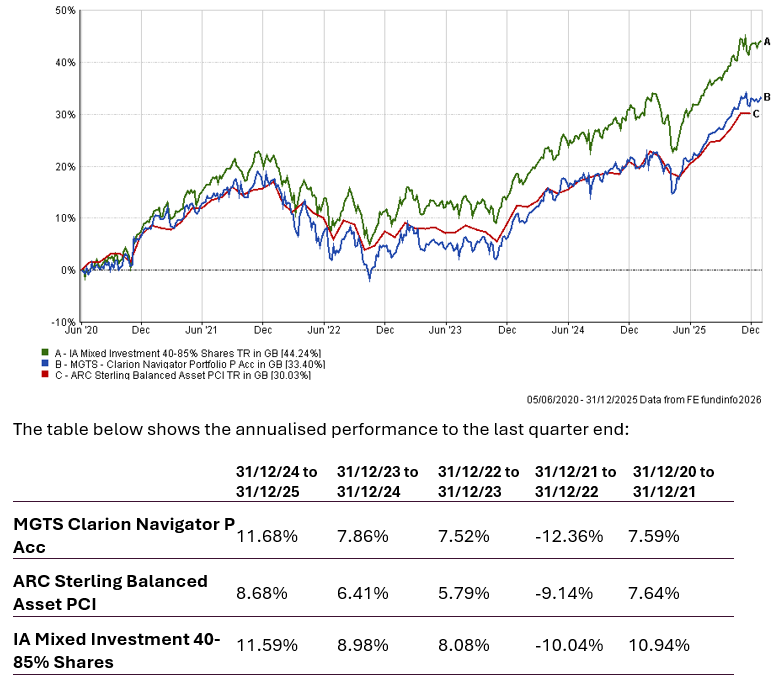

Navigator Fund

The chart below shows the historical performance of the Navigator Portfolio against a relevant benchmark since the start of the available data.

Changes to the Navigator Fund

Due to changes in the underlying strategic asset allocation, the following changes were made to the Navigator portfolio:

Equities

- L&G Global Infrastructure Index I Acc was decreased from 4.50% to 3.50%

- BNY Mellon Global Infrastructure Income F Acc was increased from 1.50% to 2.50%

- Schroder Institutional Pacific I Acc was removed from the portfolio at 2.00%

- M&G Asian I Acc GBP was added to the portfolio at 2.00%

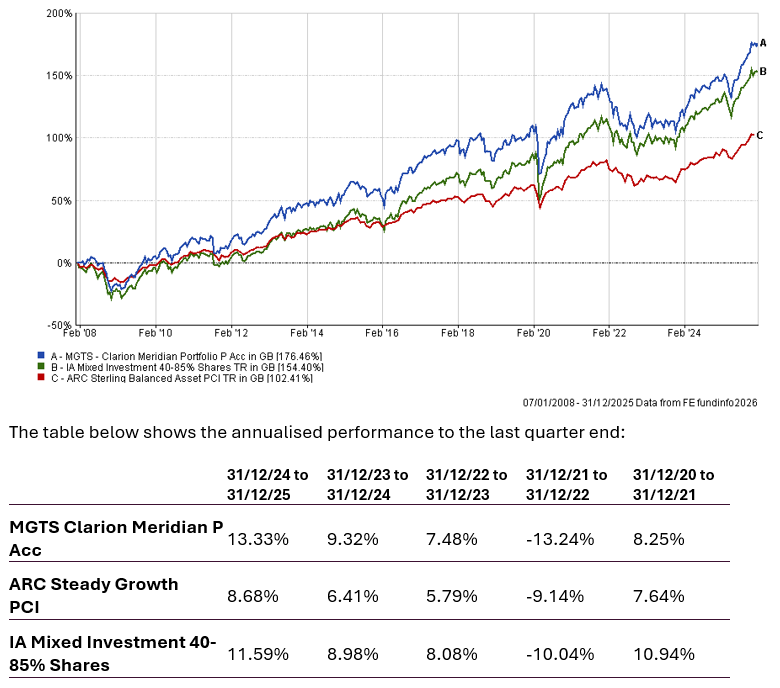

Meridian Fund

The chart below shows the historical performance of the Meridian Portfolio against a relevant benchmark since the start of the available data.

Changes to the Meridian Fund

Due to changes in the underlying strategic asset allocation, the following changes were made to the Meridian portfolio:

Equities

- L&G Global Infrastructure Index I Acc was decreased from 5.50% to 4.50%

- BNY Mellon Global Infrastructure Income F Acc was increased from 1.50% to 2.50%

- Schroder Institutional Pacific I Acc was removed from the portfolio at 2.80%

- M&G Asian I Acc GBP was added to the portfolio at 2.80%

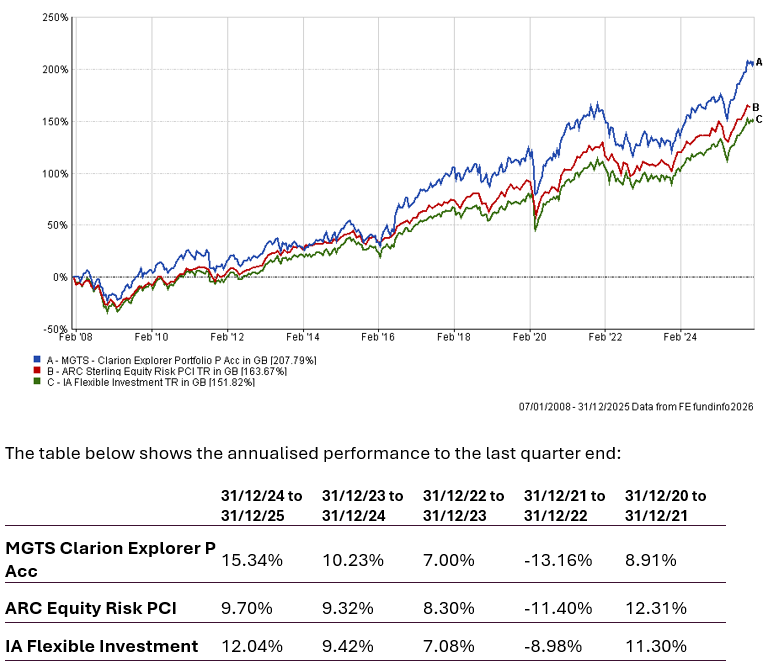

Explorer Fund

The chart below shows the historical performance of the Explorer Portfolio against a relevant benchmark since the start of the available data.

Changes to the Explorer Fund

Due to changes in the underlying strategic asset allocation, the following changes were made to the Explorer portfolio:

Equities

- L&G Global Infrastructure Index I Acc was decreased from 5.50% to 4.50%

- BNY Mellon Global Infrastructure Income F Acc was increased from 1.50% to 2.50%

- Schroder Institutional Pacific I Acc was removed from the portfolio at 4.00%

- M&G Asian I Acc GBP was added to the portfolio at 4.00%

Holding a globally diversified portfolio of high-quality assets is important to provide resilience and grow the value of savings over the long term and remains the appropriate method for allocation of investor capital. Cash is unattractive as inflationary pressures, although moderating, look to be structurally long term and real returns on cash deposits are becoming even less attractive.

Keith W Thompson

Clarion Group Chairman

December 2025

Risk Warnings

Any investment performance figures referred to relate to past performance which is not a reliable indicator of future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments, and the income arising from them, can go down as well as up and is not guaranteed, which means that you may not get back what you invested. Unless indicated otherwise, performance figures are stated in British Pounds. Where performance figures are stated in other currencies, changes in exchange rates may also cause an investment to fluctuate in value.

The content of this article does not constitute financial advice, and you may wish to seek professional advice based on your individual circumstances before making any financial decisions.