True lifelong financial planning for the serious business of life.

True lifelong financial planning

for the serious business of life.

True lifelong financial planning for the serious business of life.

True lifelong financial planning

for the serious business of life.

Category: Investment management

The Clarion Investment Committee met on 18 June. The following notes provide an overview of some of the main points of consideration in the Investment Committee discussions. They have been updated to include commentary on recent events and the wider implications for financial markets.

Please click here to access our June Stock Market & Economic Commentary written by Clarion Group Chairman, Keith Thompson.

Our investment philosophy is guided by proven financial research, applied with care by our in-house Investment Committee. We do not chase trends or make predictions. Instead, we rely on evidence, structure, and oversight to manage wealth responsibly over the long term.

We focus on what can be controlled: diversification, discipline, and costs. This allows us to create efficient portfolios designed to weather uncertainty and deliver the returns that markets provide.

Our approach is built on five enduring principles, which together form the foundation of our Investment Philosophy.

Each of the five philosophy pillars reflects our commitment to managing your wealth with clarity, discipline, and care.

1) Evidence-based investing. Disciplined, diversified portfolios deliver better long-term outcomes than chasing the latest market trend.

2) A systematic process. A structured repeatable process designed to remove guesswork and emotion.

3) Cost efficiency. We carefully select cost-effective investment solutions without compromising quality.

4) Independent oversight. Every decision is reviewed and challenged by our in-house Investment Committee, supported by Margetts Fund Management and Dynamic Planner.

5) A responsible perspective. Identifying risks and opportunities that could affect your wealth in the years to come and building resilience into client portfolios.

The recent deal between the US and Iran, aimed at ending the war that started four months ago and reopening the Strait of Hormuz, marks a significant moment for the global economy. Oil prices dropped on the news and market expectations for inflation and future interest rate hikes were scaled back.

Here are five observations on the wider implications for the global economy.

First, on the macroeconomic front, the deal aims to deliver what base case scenarios by many forecasters have already assumed – a gradual recovery in energy production in the Gulf and a full resumption of trade through the Strait of Hormuz from later this year.

Earlier this month, the OECD published forecasts for two scenarios, with one closely resembling the outcome described above in which global growth settles at 2.8% this year, down from 3.4% in 2025 before recovering to 3.1% in 2027.

Second, as recent clashes between Israel and Hezbollah, and subsequent threats from the US and Iran demonstrate, there remain significant risks to the durability of this agreement. Although the earlier scenario is now more likely to come to pass, one cannot entirely rule out the alternative, where current energy production and export issues in the Gulf persist well into 2027.

In that case, the OECD estimates global growth will fall further – to 2.1% this year – and then slow to 1.8% in 2027, which would be the global economy’s weakest performance since 1991, except during the pandemic and the global financial crisis.

Third, even with an immediate easing of shipping disruptions, oil prices will remain above their pre-conflict levels for some time. The price of crude oil is now around $80 a barrel and futures markets expect little change in that over the next six months. This compares to a pre-conflict price of around $60 per barrel.

Markets are accounting for the fact that it takes time to restart refineries and get oil tankers where they need to be. Insurance premiums for shipping are also likely to remain elevated as long as the risk of a rupture in the US-Iran talks is real. Together with the need to rebuild depleted inventories across the world, these factors will maintain upward pressure on oil prices.

Fourth, for south and southeast Asian economies, which have endured most of the energy shock, the deal should provide some respite from this historic disruption. As the destination for more than three-quarters of the crude oil moving through the Strait of Hormuz, the region relies heavily on imports from the Gulf. Over the last few months, these economies have faced significant fuel shortages, with many resorting to rationing of some form.

Even a partial resumption of supplies should lower fuel prices and reduce inventory hoarding. Major importers such as India should see a meaningful easing of inflationary pressures through reductions in transport and distribution costs. This should also create room for some central banks in the region to keep interest rates at or around current levels.

Finally, global growth has slowed, not collapsed, in the face of this unprecedented shock. Oil markets have lost nearly 13 million barrels of output per day, over 12% of global supply, dwarfing the lost output during the 1970s and 1980s shocks that triggered deep downturns. Yet even the prolonged disruption scenario from the OECD doesn’t tip the global economy into recession.

Advanced economies have become more energy-efficient over the decades, switching to a more diversified energy mix, including renewables and increased US fossil fuel production. Their strategic petroleum reserves have also acted as a crucial buffer over the last few months. Add to that the ongoing boom in AI investment and we have all the ingredients for this remarkable economic resilience.

The global economy has weathered this historic energy shock well. Yet, momentum has slowed, and there remain limits to its endurance. A meaningful resolution to the conflict with Iran should support a gradual recovery. But, as more recent events show, that is by no means a given.

It’s been four months since the war in Iran began. But its full impact on UK inflation is yet to be felt.

So far, the global energy shock has primarily raised transport fuel prices in the UK, but a cut in the Ofgem price cap, announced just before the conflict began in February, provided a significant reduction in households’ energy bills in April. Regulated service prices, many of which are updated annually in April, such as water and sewerage bills, have also seen much slower rises than last year.

As a result, headline inflation has fallen from 3.3% in March to 2.8% in April.

However, as UK consumers are gradually exposed to the effects of this energy shock, inflation will rise. The Ofgem price cap sees a big uplift in July, pushing energy bills higher. With fertiliser shortages and rising input costs, food price inflation is expected to accelerate through this year.

But the bigger risk is from second-round effects – a short-term spike in inflation risks stoking faster wage growth or encouraging firms to raise prices. That could intensify price pressures. We saw this after the energy shock in 2022, which coincided with an overheating economy and a historically tight labour market. Strong second-round effects drove UK inflation to 11.1%, its highest level since 1981.

This episode, though, is unlikely to be so severe. Despite steady growth in the first quarter, underlying momentum remains weak. With recent cost rises and already squeezed margins, businesses may have little room to absorb higher input prices. But consumer confidence and demand remain subdued. That should limit firms’ ability to push through significant price rises.

The labour market has also been softening. With job vacancies running at their lowest level in five years and corporate hiring intentions weak, this is a difficult backdrop for inflation-busting wage rises.

As a result, this inflationary episode is likely to be shorter-lived than the one in 2022. UK inflation is likely to peak at just under 4% in the autumn before gradually easing to the Bank of England’s 2% target by the end of next year.

The ECB recently published a report that found gold has overtaken US government treasuries as the top reserve asset for central banks.

This reflects strong demand for the safe-haven commodity amid growing geopolitical uncertainty and diversification away from US treasuries. It also reflects gold’s meteoric rise in recent years, increasing 115% in price since 2024 (almost triple the gains made by the FTSE100 UK equity index and nearly double the S&P 500 US equity index).

However, the price of this safe-haven asset has fallen 15% since the start of the war in Iran.

The conflict has resulted in higher oil prices and inflation, increasing market expectations for interest rates. This has raised the appeal of interest-earning assets compared to gold, which yields no income and incurs storage costs. A stronger US dollar in recent months has also made gold more expensive for non-US investors.

Does this mean the price of gold has already reached an inflexion point? Analysts think not. Strong demand is expected to continue, and, subject to a de-escalation in the war in Iran, analysts foresee a reversal in gold’s decline by the year-end.

Holding a globally diversified portfolio of high-quality assets is important to provide resilience and grow the value of savings over the long term and remains the appropriate method for allocation of investor capital. Cash is unattractive as inflationary pressures, although moderating, look to be structurally long term.

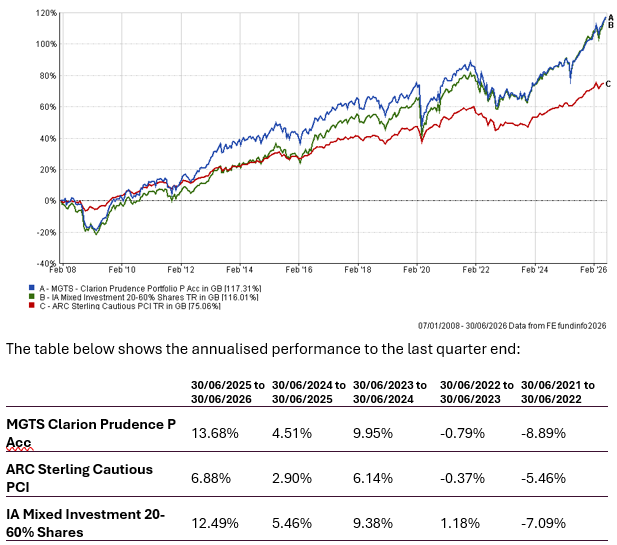

The chart below shows the historical performance of the Prudence Portfolio against a relevant benchmark since the start of the available data.

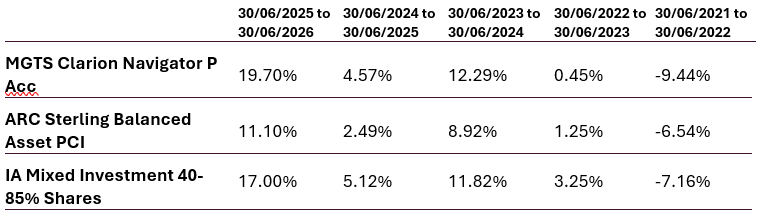

The chart below shows the historical performance of the Navigator Portfolio against a relevant benchmark since the start of the available data.

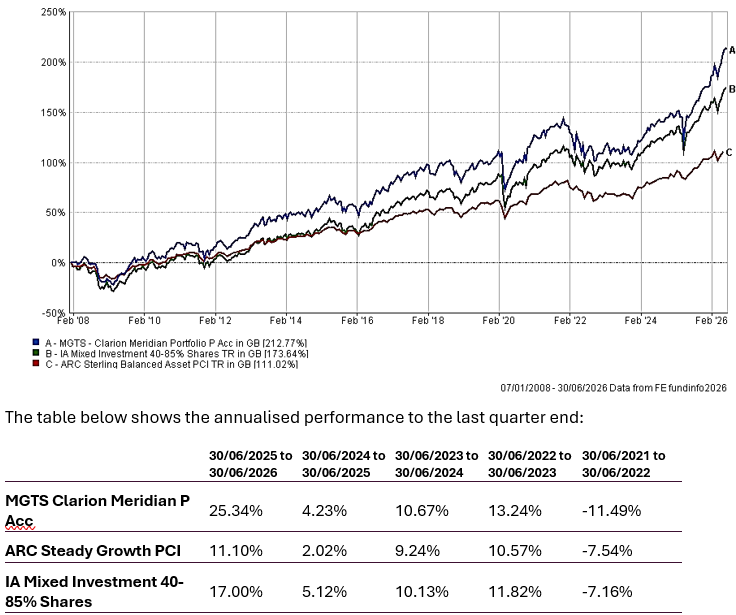

The chart below shows the historical performance of the Meridian Portfolio against a relevant benchmark since the start of the available data.

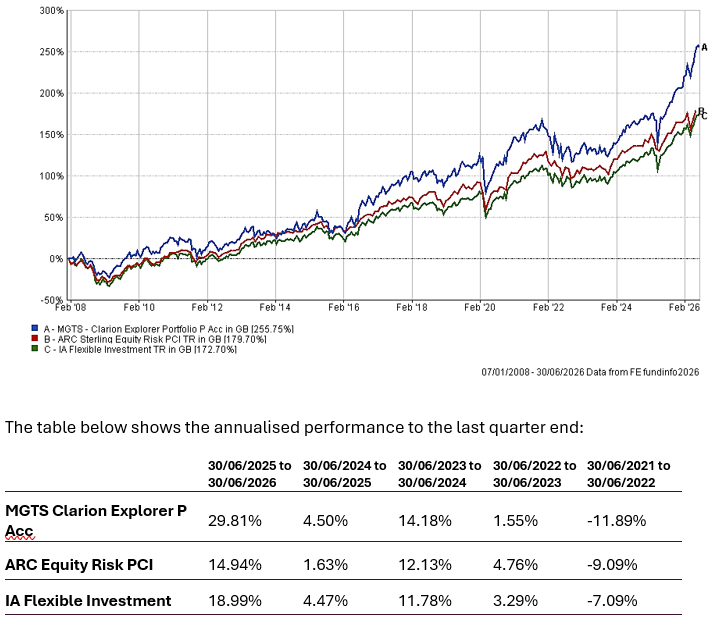

The chart below shows the historical performance of the Explorer Portfolio against a relevant benchmark since the start of the available data.

Keith W Thompson

Clarion Group Chairman

June 2026

Any investment performance figures referred to relate to past performance which is not a reliable indicator of future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments, and the income arising from them, can go down as well as up and is not guaranteed, which means that you may not get back what you invested. Unless indicated otherwise, performance figures are stated in British Pounds. Where performance figures are stated in other currencies, changes in exchange rates may also cause an investment to fluctuate in value.

The content of this article does not constitute financial advice, and you may wish to seek professional advice based on your individual circumstances before making any financial decisions.

If you’d like more information about this article, or any other aspect of our true lifelong financial planning, we’d be happy to hear from you. Please call +44 (0)1625 466 360 or email [email protected].

Click here to sign-up to The Clarion for regular updates.