True lifelong financial planning for the serious business of life.

True lifelong financial planning

for the serious business of life.

True lifelong financial planning for the serious business of life.

True lifelong financial planning

for the serious business of life.

Category: Financial Planning, Investment management

Held at Overbank, 52 London Road, Alderley Edge, Cheshire, SK9 7DZ at 13:00.

| Ron Walker (RW) | Director |

| Keith Thompson (KT) | Chair/Director |

| Dmitry Konev (DK) | Analyst (Margetts Fund Management) |

| Toby Ricketts (TR) | Fund Manager (Margetts Fund Management) |

| Sam Petts (SP) | Financial Planner (Clarion Wealth Planning) |

Minutes from the previous meeting held on 25th February 2019 were agreed by the Committee as a true and accurate account.

SEE ACCOMPANYING MARKET AND ECONOMIC COMMENTARY FOR MORE INFORMATION

This Commentary provides a general overview of the points discussed by the Committee which can briefly be summarised as follows:

Risk reports were not available, DK will distribute via email.

The Committee noted that over 10 years the performance of Explorer was broadly similar to Meridian when the Funds have different risk/return profiles. It was agreed that this performance differential can be partly attributed to the QE program which has had a significant influence on valuations of US equities, which were historically held at a higher weighting in Meridian, while Explorer had a historic tilt towards Asia and Emerging Markets.

The Committee looked at different 5 and 3-year periods, where performance profiles of Prudence, Meridian and Explorer were more in line with expectations as Explorer outperformed Meridian as would be expected. It was noted that anomaly periods where risk and performance profiles of higher and lower risk strategies could last for some time but over the long-term they tend to perform in line with expectations.

The Committee looked at the underlying allocation and fund selection in Meridian and Explorer and agreed that Explorer was higher risk and therefore, logically had higher return potential. Looking at various time periods, the Committee agreed that the funds were performing in line with expectations and their performance profiles were significantly different. A combination of good fund selection and asset allocation has resulted in superior fund performance for risk taken in Meridian.

In principle, the Committee agreed that all portfolios are managed in line with expectations and raised no concerns.

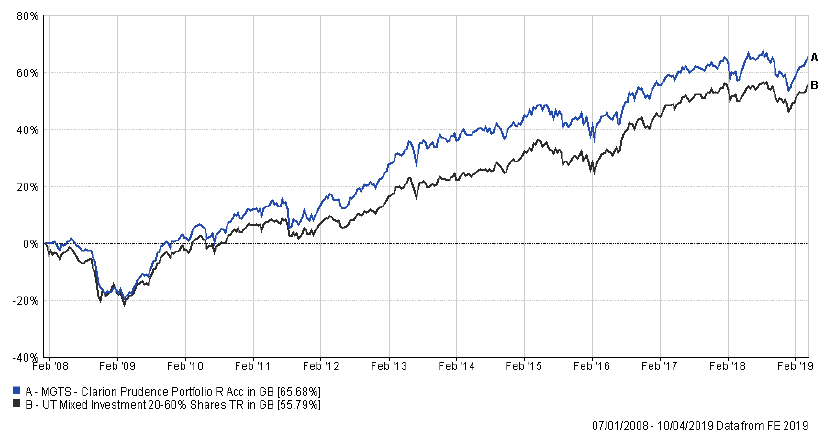

Prudence entered March on a positive note and was ahead of the IA Mixed Investment 20-60% Shares sector by c.0.7 percentage points over 3 months. A positive asset allocation effect from an overweight equity position was complemented by a strong selection of underlying equity funds and a slightly weaker performance of underlying bond funds.

In bonds, our short-duration bias detracted from performance as Gilt yields fell over the period. The Royal London Global Index Linked Bond fund was the best performing bond strategy due to the relatively long duration.

5 of the 7 underlying active funds have outperformed their respective sectors. The Franklin UK Equity Income fund was the best performing holding over 12 weeks. This fund has a relatively high bias to large-cap stocks, which outperformed mid-caps in March. The Threadneedle UK Equity Income fund was the weakest performer. This fund currently has an overweight to Industrials and was one of the best performing UK Equity Income funds during market falls in 2018, but lagged the sector on market recovery in 2019. The Committee have no immediate concerns regarding this holding given its strong long-term track record.

The Committee discussed the Aviva Investors UK Equity Income fund which was behind the sector in February, but recovered in March. The Aviva fund is relatively expensive compared to other large-cap UK strategies included in the IA UK Equity Income sector. Nevertheless, this fund is a strong long-term performer and the Committee decided to keep it at this stage but will closely review performance in coming meetings.

Overall, the Committee are happy with the performance of the Prudence fund and no changes have been proposed.

The Committee approved the strategy and confirmed it is in line with the mandate.

Similar to Prudence, Meridian had another positive month driven primarily by an overweight equity allocation. The fund selection effect had a mixed result as approximately half of the underlying funds underperformed their respective sectors.

Except for the Royal London Short Duration Global Index Linked fund, all underlying bond strategies were behind their respective sectors due to the same reasons as in the Prudence portfolio.

Asian funds were the two best performers in March lead by First State Asia Focus. Asian strategies were closely followed by the M&G Global Dividend fund. Over 12 weeks UK, US and Global were the three best performing areas.

The Committee are pleased with the improving performance of the SVM UK Growth strategy, which has outperformed the IA UK All Companies sector over 12 weeks as well as over shorter-term periods. This is mainly a mid-cap fund, has a relatively high sensitivity to the health of the UK economy and was subject to significant swings related to Brexit sentiments. This fund has struggled to outperform consistently during the last two years but subsequently outperformed as the chance of a disorderly no-deal Brexit decreased.

The Committee questioned the recent weaker performance of the JPM UK Dynamic fund. DK will request a commentary from JPM and present a review of the fund’s performance and positioning at the next IC meeting.

The SLI UK Equity Income Unconstrained was another UK holding questioned by the Committee. This fund lagged the IA UK Equity Income sector over 2 years. DK explained that this was primarily due to its mid and small-cap bias and a relatively high current allocation to Financials. TR and KT voiced concerns about Aberdeen/Standard as a company. After the merger of Aberdeen with Standard Life there has been some instability across the group and a significant rotation of investment and supporting staff. KT feels that these changes are likely to put pressure on the manager’s willingness and ability to outperform within the current framework. DK felt that given the fund’s current positioning, replacing it after a period of underperformance might not be the best solution, but accepted TR’s and KT’s arguments regarding the instability of the underlying company. The Committee agreed that given both factors, there was a sound reason to replace the SLI fund.

Given the more mid-cap nature of this fund, the Committee first looked at a number of strategies with mid-cap bias, however their performance profiles did not generate a significant amount of interest around the table. KT proposed buying the Evenlode UK Income fund, which has a large-cap bias, and which has performed extremely well compared to its peer group. The Committee looked at the performance of the Evenlode fund and its underlying asset allocations and expressed their willingness to proceed with the switch. Since the meeting DK has contacted Evenlode, who said that the fund has been soft-closed and new investors have to incur a 5% initial charge. The Committee will look at other alternatives at the next IC meeting.

KT proposed replacing a US equity tracker currently included in the portfolio with the Fundsmith Equity fund on the basis that this was one of the best performing funds in the sector, has a degree of diversification away from the US and was actively managed. TR had no objection to this change and felt that replacing a US fund with Fundsmith could reduce the portfolio’s overall exposure to the US and spread its positioning more globally. The Committee agreed to go forward with the switch and asked DK to execute it.

Overall the Committee are happy with the performance of the Clarion Meridian fund and made no other changes at this stage.

The Committee approved the strategy and confirmed it is in line with the mandate.

Explorer was ahead of the sector over 3 months and has benefited from strong fund selection which has worked well at the start of 2019 and had a relatively muted asset allocation effect.

The effect of fund selection has levelled off slightly in March as most underlying Asia and Emerging Markets funds have a bias toward quality companies. These strategies performed well during market falls in 2018, but lagged on market rises in 2019, which is in line with the Committees expectations.

The Henderson Emerging Markets Opportunities strategy was relatively disappointing as the fund fell below its sector by c.2% in March. TR explained that the fund manager has now left Henderson and the team was currently managing this mandate. The Committee discussed the fund in more detail and given the recent period of weaker performance, decided to replace it with another Emerging Markets strategy. DK proposed the UBS Global Emerging Markets fund and after reviewing its risk and performance profile, the Committee agreed to support DK’s suggestion.

KT proposed replacing one of the US trackers in this portfolio for a global fund. The Committee agreed with KT, and made a collective decision to buy the Lindell Train Global Equity fund to provide a balance and diversification to The Fundsmith purchase in Meridian. When looking closely at the underlying asset allocations of the Lindsell Train strategy, the Committee noticed that it has a quite a high exposure to Japan. The Committee did not wish to increase the portfolio’s overall Japan exposure and it was therefore agreed to reduce the portfolio’s direct allocation to Japan by 1.5%, increase the allocation to the UK by 1.5%, sell the Vanguard UK Equity Index tracker and purchase the Lindell Train Global Equity fund.

The Committee are pleased with the overall performance of this strategy and proposed no other changes at this meeting.

The Committee approved the strategy and confirmed it is in line with the mandate.

Model A

Model B

Model C

Model D

Model E

NOTE THE 5% EVENLODE INITIAL CHARGE DOES NOT APPLY WHEN ON A PLATFORM .

Model F

Model G

DK provided a review of the Fidelity Short-Duration Bond fund. The key points are noted below.

No other Business at this point and the Meeting closed.

If you’d like more information about this article, or any other aspect of our true lifelong financial planning, we’d be happy to hear from you. Please call +44 (0)1625 466 360 or email [email protected].

Click here to sign-up to The Clarion for regular updates.